Estimate your monthly payment, review the complete cost breakdown, and compare payoff options with the Mortgage Calculator.

Free to use

No sign-up

Mobile friendly

Enter Your Mortgage Details

Amortization Schedule

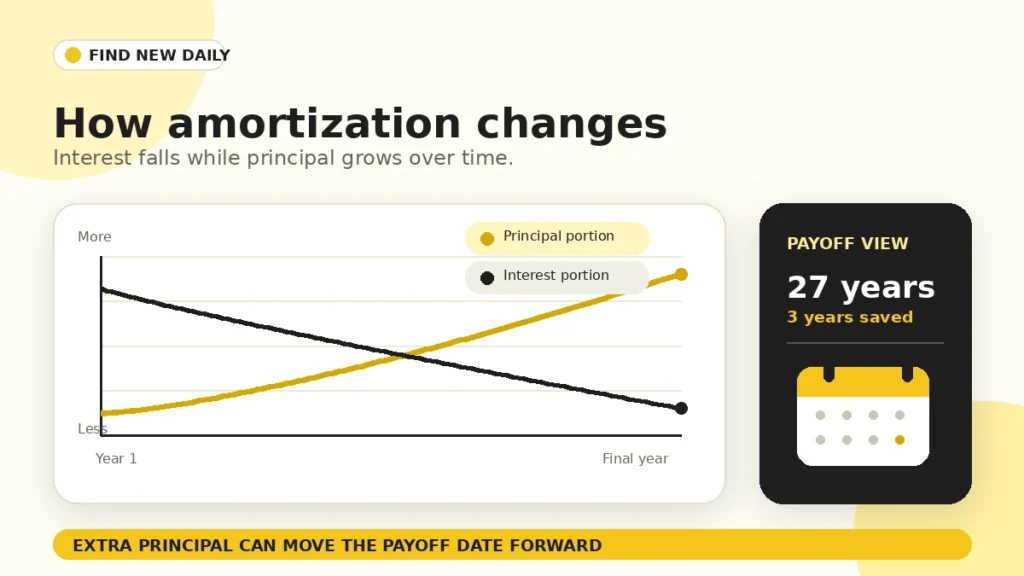

The yearly summary shows how much of your mortgage payment goes toward principal and interest each year. Monthly details can be expanded below.

Year

Total Payment

Principal Paid

Interest Paid

Ending Balance

Month

Payment

Principal

Interest

Extra Payment

Remaining Balance

Simple mortgage guide

Understand Your Mortgage Calculator Results

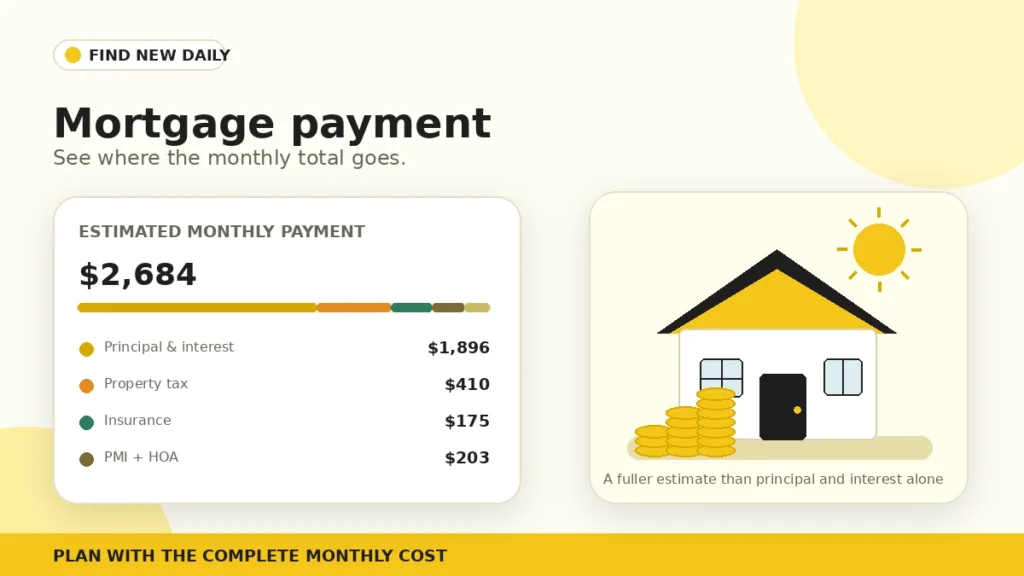

The number at the top is your estimated monthly housing cost. The cards underneath show where that money may go, so you can compare homes and loan options without guessing.

What this estimate includes

Principal, interest, property tax, homeowners insurance, PMI, HOA fees, and any extra payment you choose to add.

What may change later

Your lender's final rate, closing costs, local taxes, insurance quote, and escrow rules can move the real payment up or down.

Best way to compare

Change one input at a time. Try a different down payment, rate, or loan term and watch the total payment and interest update.

A clear payment breakdown makes it easier to see which costs come from the loan and which come from owning the property.Read the full mortgage guide

How to Use This Mortgage Calculator

Start with the home's purchase price and your planned down payment. Add the interest rate and loan term from a lender quote, or use a reasonable estimate while you are still shopping. Property tax and insurance matter because they are often collected with the loan payment through escrow.

Use the optional PMI and HOA fields only when they apply. PMI is common with a conventional loan when the down payment is below 20%, while HOA dues depend on the property. Extra-payment fields are useful when you want to see whether a small monthly overpayment could shorten the loan.

Helpful habit: Save two or three realistic scenarios rather than testing only the lowest possible payment. A comfortable payment leaves room for repairs, utilities, moving costs, and changes in insurance or taxes.

What Makes Up a Mortgage Payment?

The loan portion has two parts: principal and interest. Principal reduces what you owe. Interest is the lender's charge for providing the money. At the beginning of a typical fixed-rate mortgage, more of the scheduled payment goes toward interest. Over time, the principal share grows.

Property taxes, homeowners insurance, PMI, and HOA dues are not part of the loan formula, but they still affect your monthly budget. That is why this page shows each item separately instead of presenting only a principal-and-interest number.

Amortization shows the gradual shift from interest-heavy early payments to larger principal payments later in the loan.

Down Payment, PMI, and Loan-to-Value

A larger down payment lowers the loan amount and loan-to-value ratio. It may also remove PMI from a conventional mortgage. A smaller down payment can help you buy sooner, but it usually creates a larger monthly payment and may add mortgage insurance.

The calculator's PMI figure is an estimate based on the percentage you enter. Actual pricing depends on the lender, loan type, credit profile, and insurer.

15-Year vs. 30-Year Mortgage

A 15-year loan normally has a higher monthly payment because the same balance is repaid in half the time. The trade-off is less total interest. A 30-year loan spreads payments out, which can make the monthly amount easier to manage, although the total interest is usually higher.

Neither term is automatically best for everyone. Compare the payment with your regular savings goals and emergency fund, not only with the maximum amount a lender may approve.

How Extra Payments Affect the Loan

Extra money applied to principal reduces the balance sooner. That can lower future interest and move the payoff date forward. Before making extra payments, confirm that your lender applies them to principal and check whether the loan has any prepayment restrictions.

Mortgage Payment Formula

The standard fixed-rate principal-and-interest formula is:

M = P [ r(1+r)n ] / [ (1+r)n - 1 ]

M is the monthly principal-and-interest payment, P is the loan amount, r is the monthly interest rate, and n is the total number of monthly payments. Taxes, insurance, PMI, HOA dues, and extra payments are added separately.

Sample Principal-and-Interest Payments

These examples are illustrations only. They do not include taxes, insurance, PMI, HOA dues, or lender fees.

Loan Amount

Interest Rate

15-Year Payment

30-Year Payment

$200,000

6.00%

$1,688

$1,199

$300,000

6.25%

$2,572

$1,847

$400,000

6.50%

$3,484

$2,528

$500,000

6.75%

$4,425

$3,243

Frequently Asked Questions

Does this calculator include taxes and insurance?

Yes. You can enter annual property tax, homeowners insurance, PMI, HOA dues, and extra payments to build a fuller monthly estimate.

Why might my lender's payment be different?

A lender may use a different interest rate, tax estimate, insurance premium, PMI price, escrow calculation, or fee structure.

When is PMI usually required?

PMI is often required on conventional mortgages when the down payment is less than 20%, although exact rules vary.

Can I use the calculator for refinancing?

Yes. Enter the proposed new loan balance, rate, and term. Compare the result with your current payment and remember to consider refinancing costs.

Do extra payments always save interest?

They generally reduce interest on an amortizing loan when applied to principal, but you should confirm your lender's payment rules.

Is the result a loan approval?

No. It is an educational estimate, not a credit decision, loan offer, or financial guarantee.